The insurance market, above all others, knows the role of risk. To get the highest returns, you have to keep the risks as flat as a thin crust pizza.

What most companies fail to acknowledge is that right now, the insurance sector is balancing on the brink of one major risk — digital disruption. The urgent need for business and technology modernization poses the greatest threat to the global insurance industry over the next 2-3 years.

Much like the financial sector at large, the insurance market needs to deal with a legacy burden — the technical debt legacy systems represent today and the risk that they won’t be able to keep up with demands in the short-term perspective. But that’s just the tip of the iceberg.

Several other push and pull forces are prompting insurers to reinvent themselves. Immediately.

Shifting customer demands

Some may argue that modern consumers are digitized to distraction by the likes of Amazon. They now expect every interaction with any company to be instant, affordable, low-friction, and fully digital.

Insurers may complain and mostly stick to in-person sales. Or they may adapt and overtake distracted competitors by being available via the channels modern consumers prefer: U.S. insurance brands reached the mobile tipping point in 2019, with an average of 52% of total traffic to brand sites taking place on mobile devices. However, the numerous drop-offs in mobile site features showed that insurance brands have not adjusted well to the new landscape.

Low conversions and missed sales are just part of the deal. Companies that ignore digitization in insurance risk losing their existing customers to the tech-savvier competition. In 2020, 41% of consumers said they were likely to switch insurance providers due to a lack of digital capabilities. Ouch.

So what do digitally driven consumers expect from insurers?

- Full transparency on premiums, fees, and other charges

- New business models and personalized offerings

- Reduced barriers to digital/online interactions

- Instant online connectivity and communications

- Economy-based outcomes, not generic insurance products

- Excellent personal data security and privacy

As you might expect, 18- to 24-year-olds are the most vocal proponents of going all-digital in the insurance sector. An insurance survey conducted since the start of the COVID-19 pandemic suggests that among 18- to 24-year-old consumers:

- 58% are very likely to use digital channels to engage with an insurance company in the next 90 days

- 49% are very likely to buy usage-based insurance

- 49% are budget conscious and like to shop around online to save money on their insurance.

The younger crowd isn’t the most profitable demographic, though, is it? Hold that thought. In five years, Millennials will hold the largest fraction of disposable wealth, as Boomers will transfer some $30 trillion in wealth to them. Also, the rapidly aging population places a greater financial toll on healthcare and life insurance players. Higher premiums for the older crowd won’t offset potential profit losses.

Just to reiterate: Ignoring Millennial and Gen Z consumers today will put most insurers at a disadvantage within 5 to 10 years.

While insurers may continue to get by with their current practices for some time, the customers that will matter most in the future want insurance industry transformation today.

Intensified competition from InsurTech and digital insurance players

Digital transformation in the insurance industry has also stirred up another interesting market trend — lower barriers of entry into the sector.

In the pre-digital era, legacy insurance brands sat on a neat mountain of operational procedures:

- A network of branches

- Diverse on-the-ground salesforces

- Paper-based compliance

- In-office administration and service provisioning

Building such a physical presence from the ground up required significant investment few could afford. But with the rapid arrival of cloud computing, API programming, and real-time data analytics, new entrants can assemble the needed operational infrastructure faster, cheaper, and more effectively than any legacy company. 50% of insurance CEOs see new market entrants as a threat to growth, far more than any other financial services sector.

On-premises and on-site legacy infrastructure that once allowed insurers to stay on top is now at risk of turning into the obstacle on the path to digital transformation in insurance.

The global pandemic has further revealed that agile digital insurers and InsurTech companies are in a far better position than incumbents.

So the vexing question is this: How can legacy companies take advantage of their strong legacy core and reinvent themselves digitally?

Insurance digital transformation — selecting your tech priorities for the front, middle, and back office

Legacy insurance industry technology poses several challenges:

- It gets in the way of operationalizing customer data

- It commands high maintenance and support costs

- It restricts the ability to add innovative technologies

- It undermines customer experiences and service levels/quality

Even the simplest automation or process digitization can cause major havoc in a spaghetti system. Mustering the strength to modernize these processes is imperative for insurers who want to thrive in the short-term perspective. Read more about scenarios for modernizing legacy systems

However, every investment in new technology requires a strong business case. Implementing robotic process automation (RPA) may sound fun on a whiteboard, as the promised ROI can be as high as a 600% reduction in the meantime for process execution. In real life, however, a simple three-month automation pilot can easily turn into a 12- to 24-month derailed, off-budget initiative aimed at a problem that cannot be solved with a patchwork solution.

At Intellias, we always look for the root causes of issues and advise technological solutions that are viable for the existing infrastructure.

Not every new technology in insurance is worth pursuing for every business. But stay aware of your options. Understand what’s possible and what’s not within your current levels of digital maturity. Then assess how different technological bricks can help you build a better structure.

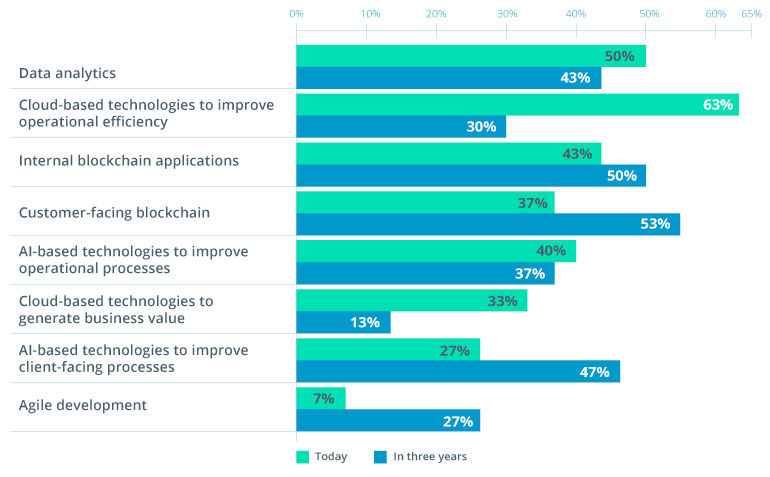

That said, let’s take a close look at what technologies have strong momentum in the insurance industry right now and are poised to maintain that momentum over the next three years:

Source: Accenture — Digital transformation is remaking insurance

Here’s how these tech trends can be translated into actual solutions that accelerate digital transformation for insurance companies.

Improved customer portals

For insurance, excellence in digital sales and customer support remains a business nuisance rather than a public convenience.

A 2019 consumer survey by TechSee reveals why insurance customers churn and cancel their contracts:

- 52% are frustrated that they had to call more than once

- 31% cite long issue resolution times

- 29% say they grew tired of dealing with incompetent, rude agents

In the digital space that the insurance sector is heading towards, customers hold more power than ever. They’re quick to research alternatives and settle for the solution that offers the best customer experience (CX) rather than go with a well-known legacy brand. Around 50% of customers were actively looking for an alternative insurer in 2019. At the same time, the other half churned passively because they were no longer satisfied with a company’s offerings/service levels or received a better offer from a competitor.

In either case, investing in a better customer engagement portal and digital retention mechanisms could reduce the churn rate.

Here’s what’s needed to support digital transformation for an insurance portal:

- Instant personalized quote tool/calculator

- Online advice tool

- Plan comparisons

- Fully digital purchase process

- Paperless onboarding experience

- Access to online professional advice

- Self-help portal and/or online chatbot

- Hotkey access to chat/phone support

Borrow some lessons from banks on how to approach front-office transformations

Blockchain-based systems

The blockchain has emerged as a strong contender for streamlining data exchanges, securing customer data, and increasing the dwindling customer trust in the insurance industry. Immutable, transparent, and distributed blockchain-based insurance applications can help optimize both internal and external processes:

Internal blockchain app use cases:

- Automated claims triggering, processing, and management

- Streamlined contract management lifecycle

- Decentralized customer data storage

- Blockchain-based KYC

Customer-facing blockchain use cases:

- Event-triggered smart contracts

- Real-time, individualized quotes

- On-demand, usage-based insurance and microinsurance

Automated claims management systems

Lack of unity in back-office functions in terms of processes, governance structures, and data syncing drive up operational costs for insurers and undermine customer satisfaction at the same time. Spring cleaning those operational processes and introducing a greater degree of automation can help legacy insurers catch up with fully digital players.

Robotic process automation in claims management can lead to:

- Cost reductions

- Fewer errors

- Productivity savings

- Underwriting efficiency

- Claims efficiency

More mature tech companies should also look into emerging artificial intelligence (AI) and machine learning (ML) use cases. Cognitive claims management systems, powered by real-time data analytics and machine learning algorithms, can:

- pre-assess claims to automatically evaluate damage

- detect elaborate fraud scenarios

- predict claims volume patterns

- perform advanced loss analysis

- fully manage the entire claim management lifecycle.

During a recent pilot, AI algorithm successfully executed the entire health insurance claims process from receiving a claim to recording the closure in 11.5 minutes without any human intervention.

Telematics and personalized insurance

The auto insurance sector is particularly ripe for innovation, as most new cars come installed with ADAS systems and other connected functionality, producing tons of valuable data both for drivers and insurers.

Capturing and operationalizing such telematics data enables insurers to offer truly personalized usage-based insurance (UBI) or even venture into new pay-as-you-drive business models that reward drivers for safe behavior with better premiums and special discounts.

Further, with the growing number of connected things, insurers could personalize every other product in their portfolio to a customer’s (or business’s) way of going about their day.

- Healthcare and wellness wearables can be used to deliver personalized healthcare insurance plans and premiums.

- Smart appliances such as connected security alarms can provide extra data for renter and homeowner insurance providers.

- Telematics data can be used to adjust commercial insurance plans for fleets.

- Location-based and drone data can help improve insurance plans for agricultural businesses.

A strong insurance digital strategy can help auto insurers best serve their clients’ needs across generations while growing their income.

To conclude

In the world of insurance, digital strategy is a locus of profound pressure and anxiety. The pressure is high indeed, but so is the need to make smart decisions when it comes to new tech investments.

Sustainable digital transformation in the insurance business requires step-by-step planning and a deep understanding of the current state of your infrastructure, backed by some insights on the feasibility and ROI of various new solutions.

The Intellias team would be delighted to work with you to see how your insurance company should approach digital transformations and which technologies will add the most value to your operations in the short- and long-term perspectives. Contact us!