Back in the day, everyone had one trusted bank account and a branch manager to dole out money on demand. In the second decade of the twenty-first century, that’s a hard scenario to imagine. Even the average unbanked and underbanked consumer uses several alternative financial accounts. Your average Millennial (and even their progressive Boomer parents) carries multiple cards, holds several investment accounts, uses investment apps, and sends money using any method but a bank.

Today’s financial industry has no lack of solutions. Amidst the range of choices, modern consumers may start feeling that less is more and steadily drift toward account aggregation.

What is account aggregation?

Account aggregation is the process of housing all of a consumer’s financial data under one roof.

In essence, account aggregation services act as universal connectors, pulling transactional, savings, investment, tax, and credit data together into one virtual warehouse that can then be plugged into any type of financial application:

- Budgeting and personal finance management apps

- Intelligent decision engines

- Wealth management platforms

- Lending portals and credit scoring systems

- Investment and portfolio management tools

- Retail banking applications

Think about how your email account is the hub for so many things in your life — personal and business communication, PayPal purchases, Venmo transfers, Uber rides, and late-night sushi orders.

Account aggregators attempt to assume the same role but offer an even more granular view into all financial aspects of your life from a single dashboard.

Being this keyholder to all customer data gives account aggregation services an upper hand on the financial market. They can drive extra value through:

- building partnership agreements with incumbent and FinTech players

- deploying value-added products and services to consumers

- capitalizing on customer analytics and insights.

Furthermore, account aggregation apps are driven by the network effect — the more integrations they offer, the more valuable they become for new partners and end users.

Considering that most intermarket competition is happening at an ecosystem level, assuming the role of an aggregator may be a winning move for some companies.

The ability to build, manage, and collaborate in complex business ecosystems will be a major competitive advantage in the decade ahead. Already, 83% of digital ecosystems involve partners from more than three industries.

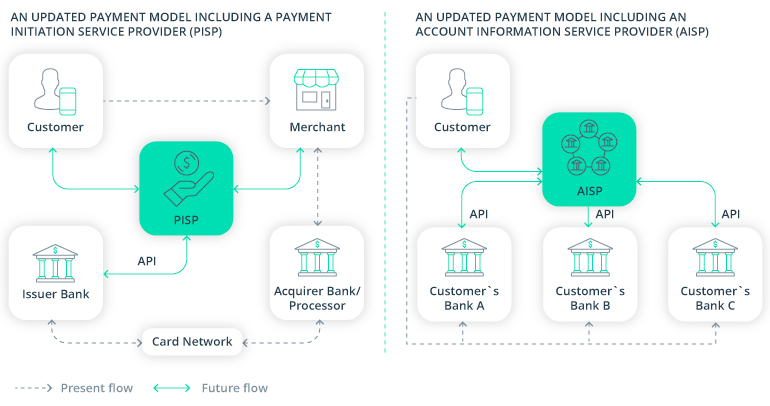

Account aggregation versus or plus open banking?

The concept of financial account aggregation is further connected with open banking.

The key premises of the open banking movement are as follows:

- On-demand, real-time data sharing enabled via APIs

- Permissioned access to any type of transactional, payment, or credit data

- Sharing requests can be initiated by both financial and non-financial players

In short, open banking promotes a greater degree of bank account aggregation arrangements that allow customers to cherry-pick the best offers from the market and build a personalized financial hub based on their needs. And that’s exactly what the modern connected consumer demands.

The open banking trend was slow to take off, but as we predicted in our top FinTech trends for 2020, its time has come.

This year, Revolut became the first digital bank to hop on the bandwagon. Revolut customers in the UK, Ireland, and Italy can now enjoy open banking account aggregation and plug in their accounts from third-party banks. Monzo is playing catch up and recently announced that they plan to offer account aggregation functionality as part of their premium Monzo Plus plan.

Indeed, the UK has become the hotbed for open banking. As of January 2020, there were 204 regulated open banking providers registered in the country. Some have even teamed up to set their own API standard for connectivity.

The rest of the world is watching closely and taking action.

Australia already has two authorized open banking players and 39 more entrants waiting for legislative approval. Frollo is one of the two early accredited FinTech players to extend SaaS account aggregation technology to both financial and non-financial partners. One connectivity provider can fuel further open banking ecosystem growth and multiply the network effect.

The European Open Banking movement, backed by the revised PSD2 directive, is growing too with some 6,023 trusted third-party payment service providers registered in the European Economic Area.

Source: Accenture — Seizing the Opportunities Unlocked by the EU’s Revised Payment Services Directive

Two years into open banking, two major account aggregation platforms — TrueLayer and Salt Edge — have gained the growth momentum for personal finance management and coaching apps, lending solutions, and especially for mortgage and investment products.

Traditional banks are also cautiously tapping into API programming in search of new revenue streams. Commerzbank, for example, is capitalizing on the open banking movement to offer usage-based loan repayment plans for capital equipment using IoT data.

In the US, the concept of open banking hasn’t been formalized at the regulatory level. Yet the account aggregation trend is still going strong in the wealth management and crediting sectors.

Wealthfront, Betterment, and SoFi, among others, are adding to their connectivity capabilities, allowing customers to connect more financial accounts to get an even deeper view of the state of their affairs.

Credit scoring tools and lending platforms are also joining the fray. Even traditional players such as Experian and FICO have recently started accepting alternative credit card data to improve their scoring algorithms.

CreditKarma has gone a step further and said that they plan to further expand their already massive set of connected data sources and accounts to improve their algorithmic financial advisory systems and accelerate the future of autonomous finance.

In China and Southeast Asia, account aggregation software lies at the heart of the most popular (and profitable) super apps. Beyond financial accounts, super apps such as WeChat, Ant Financial, and GoJek host social media, e-commerce, and lifestyle accounts under one roof and use aggregated customer data to deliver truly personalized financial services, from credit scoring to lending, rebates, and more.

The takeaway: Your average customer now has multiple current/checking accounts and uses several FinTech apps. Paradoxically (or not), they now want to manage all of their affairs from one place.

Account aggregation can help pack all of a consumer’s financial products into a single hub and allow aggregator products to own all the benefits that come from being the ultimate master key.

Why does it pay to aggregate financial accounts?

For a long time, the popular lore in the financial world was this: more services equals more value.

Then came digital banks, who changed the narrative to unbundling is the new cool, wooing consumers with affordable and effective monoline offerings. But with more FinTechs entering the space, this financial monoculture started losing its popularity. All players (digital and incumbent) started losing profit to savvier competitors offering yet another cool adjacent financial service to consumers.

With that came the current era of bundling back and mergers and acquisitions between banks and FinTechs. Mature companies have started rapidly growing their portfolios, either through in-house product development or by pursuing the marketplace banking business model.

Traditional financial institutions have also started consolidating forces and seeking partnerships with FinTechs that do one thing (lending, credit scoring, cross-border payments, investing) better than they do. Visa’s recent $5.3 billion acquisition of Plaid — an account aggregation platform with financial APIs and connectors — only proves that we’re at the cusp of a bigger shift toward aggregation.

In between these battles stands a somewhat confused customer — still loving the variety of financial products on the market but feeling more confused than delighted at the sheer volume of choice.

Millennial customers don’t think about your banking products. They’re first considering their needs.

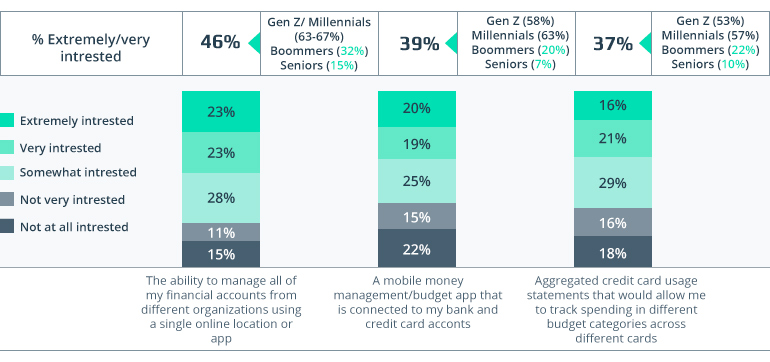

What most customers want now is a simple solution for connecting their finances (just like they connect all the other online services they use):

Source: Payments Journal — How Consumers and Companies Benefit from Data Aggregation

Meeting customers’ demands to aggregate accounts results in several hard-to-beat benefits:

- Higher revenue. Companies that provide account aggregation services earn an average of $2,000 more per customer.

- Improved customer satisfaction. Customers receive better value propositions, personalized upsells/cross-sells, and personalized advice based on aggregated data.

- Deeper customer engagement.Personalization drives customer longevity in finance and helps prevent account switching.

- Integrated product development. Having a full picture of a customer’s current standing and future aspirations lets you shape a better product strategy.

- Enhanced productivity. Your front office staff can deliver better service and remain more productive with instant visibility into all customers’ accounts.

Residual risks of account aggregation services

The decision to aggregate accounts (or not) often boils down to compliance.

Empowering customers to share access to their data can bring both benefits and liabilities. Regulations are the last thing on customers’ minds when it comes to doling out personal credentials. Data from The Clearing House 2019 survey proves that:

- Among 54% of US customers who use money management apps, 80% are not aware that these apps may store their bank account details.

- Only 21% of customers are actually aware that aggregation apps will maintain access to their personal data until they revoke that access.

Clearly, this is problematic, as customer privacy and consent is the pillar of successful banking operations. The responsibility to ensure this privacy and obtain this consent rests on the shoulders of the company offering account aggregation services, not on the shoulders of other participants or the customers themselves.

Next comes the question of the security of the aggregation platform. While many open banking initiatives promote unified API standards and authentication frameworks, we’re still miles away from having truly unified standards for data aggregation.

As a result, to aggregate accounts, companies are often forced to:

- carefully assess existing API integrations against existing security, networking, and compliance practices

- standardize certain APIs to meet set criteria and incorporate extra security measures (e.g. data encryption)

- harden and modernize the architecture of legacy banking systems to accommodate new external integrations without undermining security.

Last but not least comes the need for a strong data governance platform — the technical control panel to back your customers’ financial hub. Knowing where all aggregated data resides, who has access to it, and how it’s being used and analyzed is crucial for ensuring the security and compliance of your operations.

Account aggregation infrastructure requires constant monitoring and proactive risk management to ensure the quality (and security) of your operations doesn’t deteriorate. So make sure that you:

- have established practices for vulnerability management

- perform regular patching and strengthen platform resilience

- use traffic monitoring solutions to manage operational/security concerns

- incorporate the necessary technological means to prevent data breaches.

To conclude

Account aggregation carries its risks, but the benefits of becoming the single last step in your customers’ financial data management majorly offset the technical difficulties of getting an account aggregation solution off the ground.

Compound this with the fact that revenue erosion caused by other financial players will only grow going forward and multiply that by the fact that customers’ demands for leaner financial management are not going anywhere and the equation becomes clear:

Account Aggregation × Value-added Services = Future-proof Operations

Contact Intellias financial specialists to understand the scope of transformations your company needs to undertake to move forward with account aggregation.