Business banking will not be the turf of traditional banks for much longer. Digital banks have successfully taken over retail banking, and now they’re full speed ahead into the business banking market.

And they’re more than welcome. Small and medium-sized enterprises (SMEs) — a growing power globally — have long been underserved and unimpressed with the products offered by traditional banks.

Interest in digital business banking

Worldwide, 56% of SMEs already trust their finances to challenger banks according to the EY Global FinTech Adoption Index. In some emerging markets such as China, where traditional financial services are particularly lagging, adoption has soared to 92%.

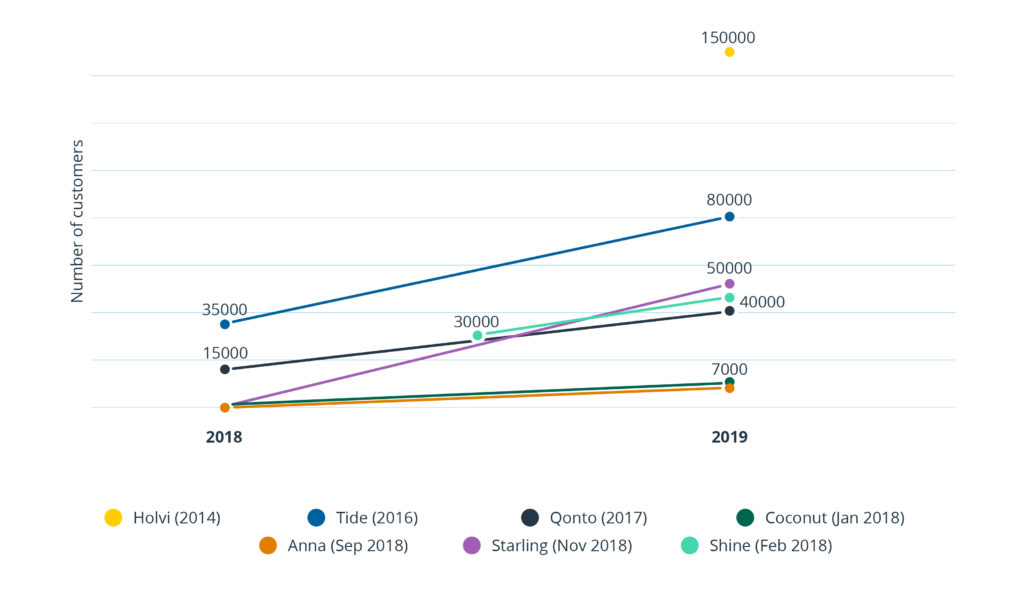

In Europe, SME banking startups have also risen in popularity. Key players have managed to accumulate five- to six-figure customer bases in less than five years:

Source: Sifted – Comparison of online business banking startups

The Intellias team decided to investigate this matter and determine what makes digital business banking accounts so attractive to SMEs and what features are a must-have for a successful launch.

Essential features for digital business banking

Early market entrants disrupted the market with a “business banking, but better” experience powered by new-gen technologies (big data analytics, machine learning, artificial intelligence, etc.).

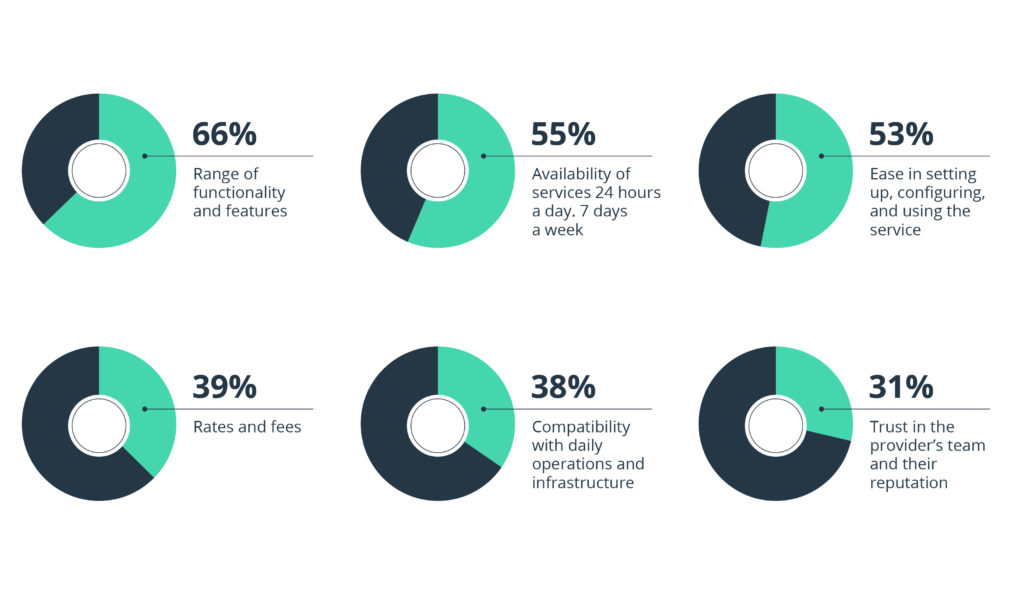

Effective KYC and onboarding, round-the-clock availability, and an expanding array of features strike a chord with business customers:

Source: EY – EY Global FinTech Adoption Index

We analyzed voice of customer data from current business banking users and concluded that the following product features are in the highest demand.

1. No-fee business current/checking accounts with multi-user access

Digital banks have set the bar for no-fee personal accounts. Business customers now expect the same perk.

Key market players (Monzo, Starling, Revolut, N26, Tide) oblige and do not charge any fees for:

- Domestic payments and transfers

- Card payments

- Account and debit card use

- ATM withdrawals (capped at a certain amount)

The second most requested business bank account feature is multi-user access, as it’s no longer just freelancers and sole traders who favor digital banking solutions.

The best strategy for meeting the needs of all these customer segments will be enabling secure, permissioned multi-user access. You can allow the account owner to invite additional users with read-only permissions (for instance, an accountant and payroll manager).

Revolut has gone a mile further, letting account owners add as many people as needed with defined roles and exercise control over their ability to:

- See and edit the account profile

- Create accounts, transactions, counterparties, cards, and payments

2. Low-cost and fast transfers

Getting paid or receiving funds should be a fast, secure, and efficient experience. SMEs are ready to switch from their traditional banks to a new digital offering if they’re provided with the following money transfer options:

- Free domestic transfers and competitively priced cross-border payments (without any hidden fees)

- Automated transfer execution and scheduling

- Direct debit management functionality for incoming and outgoing payments

- Standing order management

- Batch and recurring (subscription) payments

- Simple and fast process for adding new payees/suppliers

3. Corporate cards: debit, credit, and virtual

Source: Monzo Community

Small or not, businesses often need access to multiple cards for managing different types of expenses and day-to-day payments. The basic requirements of business users are:

- Affordable ATM withdrawals

- Contactless payment functionality

- Instant notifications for every transaction

- Virtual cards

- Cross-bank exchange rates for spending in foreign currencies/abroad

- Preapproved overdrafts with low interest rates

- In-app card security and limit controls

For digital banks, it may be tough to balance the no-fee offering with unlimited (or 10+) physical cards. Hence, to stay on the profitable side, you may want to consider either of the following options:

- Create a higher cap for virtual cards that can be assigned to different users/for different purposes

- Add a higher physical card ordering cap for certain customer segments (large businesses) or premium account holders

4. Apple Pay and Google Pay integration

Last year, nearly half of all payments in the UK were contactless. This major increase is attributed to a 114% rise in the use of Apple Pay and Google Pay among both consumers and businesses.

Beyond meeting consumer demand for this payment option, Google Pay and Apple Pay integration can also serve as a great middleware solution to supporting multiple business cards. In this case, the physical card can remain with the account owner while another user can pay via their mobile wallet.

5. Business and employee expense management

Did you know that British SMEs collectively lose over £8.72 billion per year as a result of the time taken by weekly company expense management?

Helping SMEs reclaim these hours will win your digital bank a lot of points. Basic expense management functionality should include:

- Real-time overview of all recent transactions and upcoming direct debits/scheduled payments

- Expense tracking and analytics

- Streamlined process for approving employee transactions and expense reimbursement requests

- In-app uploading of expense receipts (photo, text, or PDF)

- Different payment thresholds and reimbursement caps for employees

- Allowable and non-allowable business expenses that will be automatically rejected

- Automatic syncing of expense data with selected accounting partners

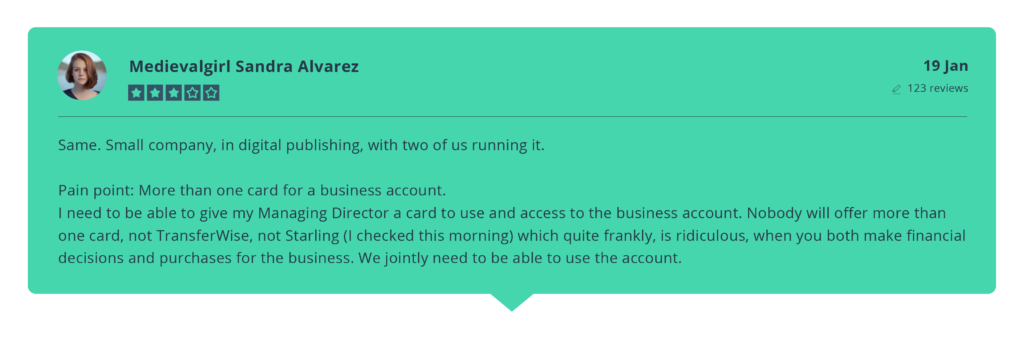

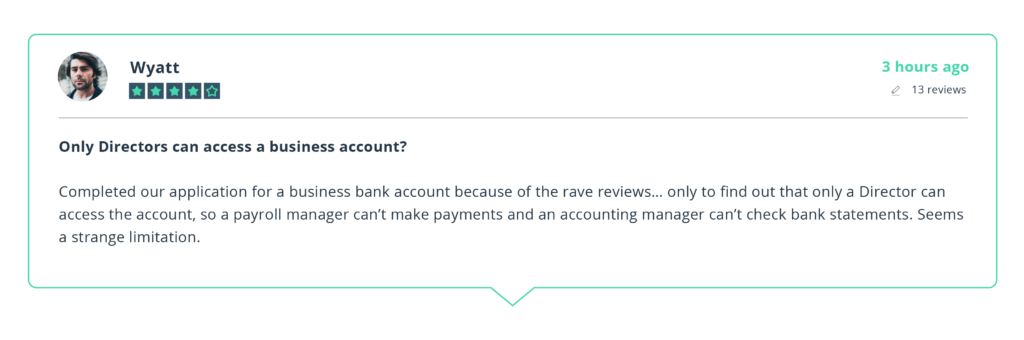

Finally, don’t forget to enable shared view access to the expenses tab — if you don’t, you’ll risk alienating some users:

Source: Trustpilot

6. Accounting software integrations

Accounting is yet another “delightful” chore that SMEs want to streamline. Your best bet is to launch your business product with:

- CSV/QIF exports

- Open APIs for reading transactions

- Direct integrations with accounting software tools

The most highly requested integrations are with Xero, FreeAgent, QuickBooks, Sage, Wave, Kashflow, and ClearBooks.

7. Exportable statements, reporting, and analytics

Real-time transaction data and instant notifications about incoming/outgoing payments are a must. Beyond that, you should offer general account analytics showing spending data, upcoming and recurring payments, and granular transaction data.

If you plan to offer a web interface for your product (which most business users request), you should also include additional transaction management features such as advanced search and filters (type, date, user, etc.), as well as standard and custom categories.

Additional top-of-mind account analytics features include:

- Exportable daily/weekly/monthly PDF and CSV statements

- The ability to create custom expenses/budget categories for different types of accounts or projects

- A premium option to request a printed and signed bank statement

8. Simple deposits

Injecting new business capital should take a few clicks or swipes. Most digital banks allow instant top-ups via debit/credit cards or bank transfer.

Some players (Starling, Monzo, and Novo) also support affordable cash/check deposits either via a partnering institution (e.g. PayPoint, the US Postal Service) or by snapping a quick picture of a check and submitting it via the mobile app (Novo).

9. Invoicing

Whether digital banks for businesses should offer in-app invoicing functionality is debatable. Most users vote in favor, but some argue that banking and invoicing should remain two separate products for convenience’s sake. Those who oppose the integration largely fear that invoicing will make an existing product more clunky and confusing.

Your best bet is to start small and test the waters with basic in-app invoice functionality, perhaps limited to only the web interface. Alternatively, you can offer a curated list of invoicing integrations via a marketplace, giving users the ability to select their favorite solution and link it with their business account.

If you do decide to move forward with in-app invoicing, consider adding the following features:

- Custom invoice numbering

- PDF exports

- Due date and invoice payment terms

- The ability to add new customers and save their details for future invoices

- Automated sending

- Automated payment reminders

10. Tax preparation

The average small business spends 12 working days per year on taxes and compliance. And those who are lax often miss important deadlines or don’t save in advance for upcoming bills.

There are several things you can do to delight business users when it comes to taxes:

-

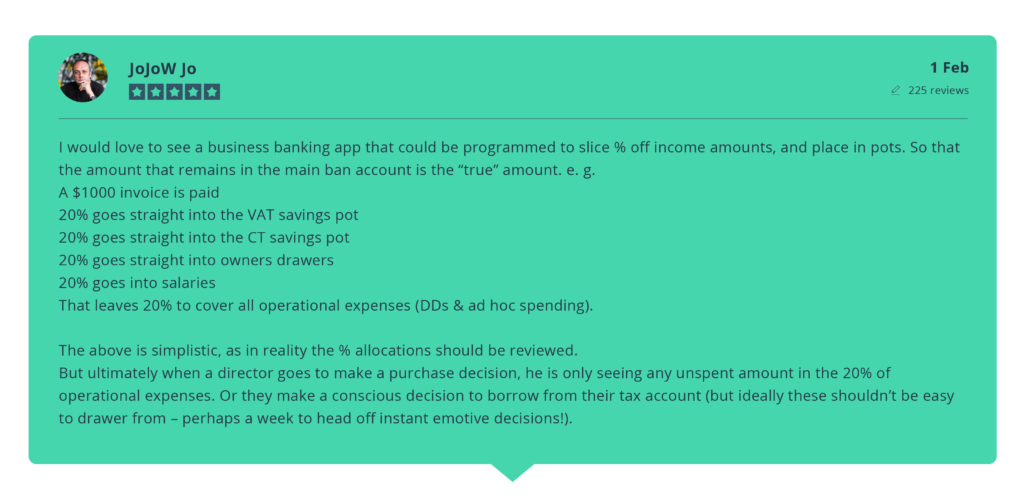

- Introduce tax savings pots/spaces like Monzo, N26, and Starling do. Let users automatically allocate a certain percentage of their income towards the tax bill(s).

Source: Monzo Community

- Estimate tax liability – Analyze the data and project how much a business should expect to pay this year depending on their incorporation type and turnover.

- Add support for direct tax payments to local authorities.

- Tax consultancy can be provided as a value-added service to select members.

Summing up

Digital banks have already found an early loyal customer base. But during our research, we noticed another interesting trend.

Digital-savvy business owners want more than a banking solution. They want a solid partner who’s capable of meeting a variety of their financial and operational needs. In the second part of this series, we’ll take a closer look at advanced business banking account features that mature users demand. Plus, we’ll dive deeper into how digital banks for business can scale their offerings by leveraging the marketplace banking model.

Stay tuned!

Intellias is an end-to-end financial software partner offering a full spectrum of product development services, from ideation to deployment. Let’s discuss how you can build and scale your digital business banking products.