A wave of innovation has transformed the financial services sector in recent years. Banks have morphed from traditional brick-and-mortar institutions to modern, tech-driven platforms that empower customers to help themselves.

Powerful technologies such as AI, machine learning (ML) and predictive analytics enable banks to anticipate customer needs and provide personalized experiences. At the same time, open banking has unlocked new opportunities for collaboration, enabling banks to integrate directly with third-party service providers. This has paved the way for a new banking business model: Marketplace banking.

In this blog post, we’ll cover everything you need to know about this exciting trend, including:

- What marketplace banking is and how it relates to open banking

- How to build a digital banking marketplace

- What digital banks currently offer — and where they can improve

- How Intellias can help you build a banking marketplace that drives growth and revenue

Ecosystems and marketplaces provide the ideal space for banks to meet customers’ needs by onboarding partners and facilitating the end-to-end delivery of offerings.

What is marketplace banking?

Marketplace banking represents the evolution of banks from standalone service providers into dynamic platforms that connect customers with a broad ecosystem of products. Banks become the central hub of a financial services marketplace where customers can pick and choose from a variety of financial products — both from the bank itself and from third parties — all within the same intuitive interface.

So, what does this look like in action? Picture a bank where you can open an account, compare mortgage rates from multiple lenders, invest through a robo-advisor and even buy insurance — all without leaving the app.

We’re building a banking experience fit for the 21st Century, where the best financial products are available securely in one place.

The idea of marketplace banking is growing in popularity, with digital-only banks like Monzo, Starling and Revolut seeking partnerships with exciting FinTechs. But the idea of platform-based banking on a mobile device originally arrived from the East, where the “so-called” BAT (Baidu, Alibaba and Tencent) triumvirate took over the retail banking sector in one quick swipe.

WeChat is perhaps the original “poster child” super app, showing how a tightly-knit ecosystem of financial, social and lifestyle services can be neatly packed into one platform.

Using WeChat wallet, users can pay for a range of goods and services — both online and in real life. One quick QR code swipe and you are done with the checkout. Spending money online is even easier. WeChat payments are accepted by all major e-tailers. Better still, you don’t need to leave the app to get what you need.

What role does open banking play in marketplace banking?

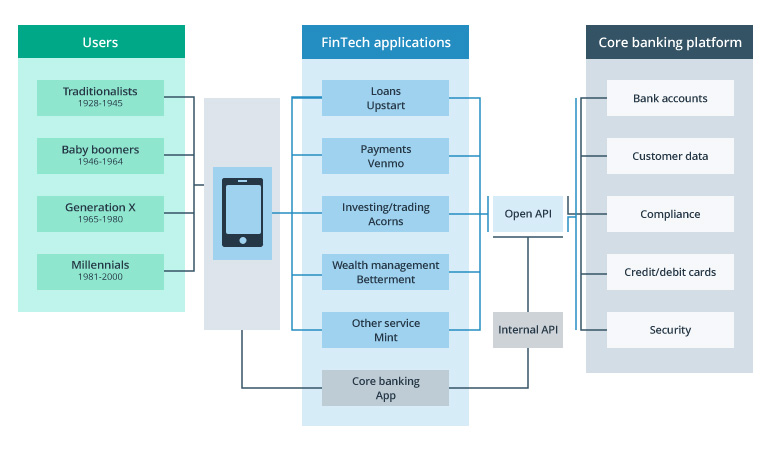

Open banking provides the technical infrastructure for marketplace banking — i.e. secure, standardized APIs that enable financial institutions to share customer data with trusted third-parties. This breaks down traditional technological barriers, enabling open and connected ecosystems and access to real-time data.

Thanks to open banking, modern banks can take an API-first approach that provides customers with a broad range of services in one place. Take British challenger bank Monzo, for example. By focusing on API-powered services and exceptional UX, it grew its customer base from around half a million in 2018 to more than 3 million in 2019. By 2024, the bank had almost 10 million customers.

The trend towards API marketplace banking is only going one way. In 2025, the number of open banking API calls is estimated to be around 137 billion. By 2029, that number is forecast to grow to 722 billion — an increase of 427%.

Marketplace banking builds on the foundation of open banking. It transforms digital banks into vibrant platforms, offering customers a diverse range of financial products and services. Banks can now integrate a broad range of offerings, including:

- Loans and mortgage brokering

- Insurance services

- Investment products and tools

- Pension products

- Accounting tools

- Budgeting and financial planning tools

The rise of the banking marketplaces

As e-commerce giants like Amazon and Alibaba have shown for decades, digital marketplaces are incredibly powerful. Through a huge variety of product offerings and services, they provide an unbeatable level of convenience, becoming a one-stop-shop for consumer needs.

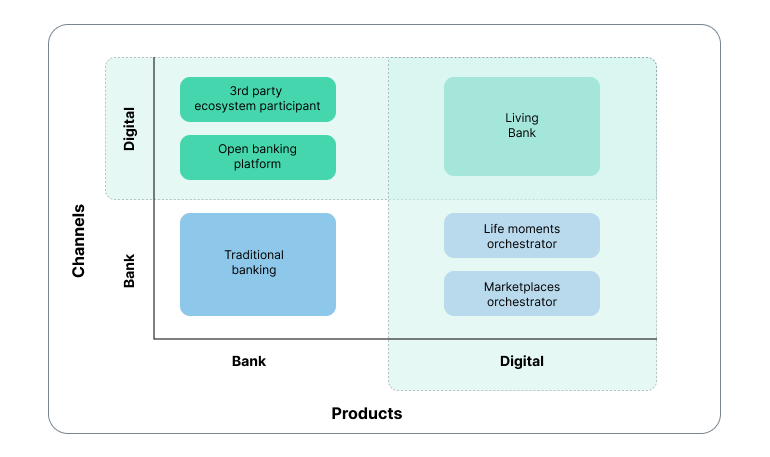

What Amazon and Alibaba do for shopping, banks can do for financial services — offering a digital hub where customers can pick and choose the financial products that suit them best. This idea is sparking a banking revolution, with an increasing number of banks transitioning from legacy high-street institutions with limited services to fully digital ecosystems, with a myriad of exciting products to choose from.

When banks realize this transition, they become what Accenture calls a “living bank”. According to the professional services giant, living banks are “consistently relevant to their customers,” and “embed vitality by delivering that hyper-relevant, ‘me-centred’ customer experience across a range of physical and digital channels.” This is achieved through data analytics, which allows banks to understand what customers want and need in real time.

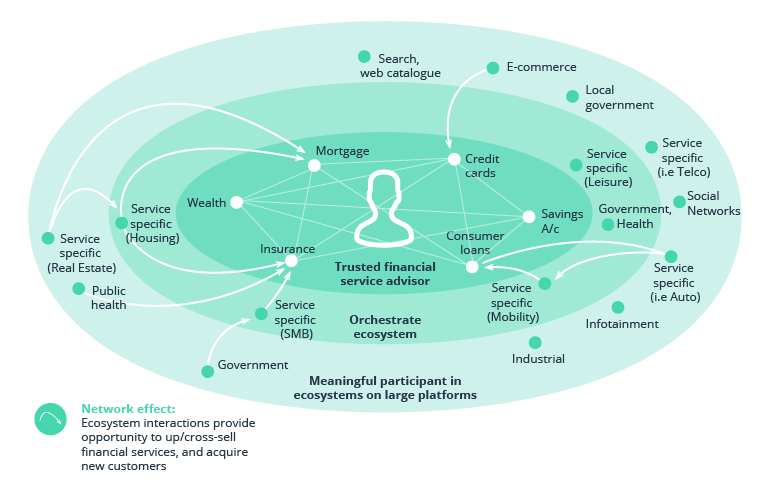

Marketplace banking is the logical endpoint of this journey. It enables banks to become the center of a technological ecosystem, where a multitude of third-party businesses, public sector organizations and services interact seamlessly. Banks can leverage these connections to create a network effect that drives growth through up-selling and cross-selling, underpinned by an incredible customer experience.

Product lessons FinTech banks should borrow from TechFins

After the initial phase of rapid customer growth, the pressure is now on challenger banks to innovate and expand their customer base. Their maturing customers are now demanding additional services on par with what traditional high street banks offer — but packaged in a slick mobile “wrapper” and at a lower cost.

New banking features and services can be built in-house. But with it becoming increasingly easy to integrate partners into your ecosystem, is developing additional proprietary products worth the time and money? The short answer is probably not.

Most customers will choose the lowest-priced, most-trusted option when it comes to products such as credit cards, savings accounts and general insurance. These are exactly the type of offers you can add to your digital banking ecosystem through partnership deals and third-party APIs. And with open banking and PSD2, it’s never been simpler from a technology or compliance standpoint.

How to develop marketplace banking

The majority of FinTech startups already have a solid base – the core financial app – that fulfills the customers’ basic financial needs. The most progressive players are now shifting their attention towards delivering even more value to customers with digital banking innovations. They are choosing to “outsource” more resource-heavy aspects of service delivery such as KYC, identity management or regulatory compliance for new types of financial products to third parties.

If your goal is to rapidly deliver a more diverse product portfolio for an affordable price, building a marketplace bank makes perfect sense. By choosing an integration-first approach, your team doesn’t need to create new infrastructure to support certain offerings. Instead, they can focus on devising additional value from the influx of customer data.

For customers, the appeal of platform banking is enormous too. Instead of being limited to a few selected products, they can shop around in a digital banking “app store” and personalize their banking experience.

85% of consumers name personalization as an important prerequisite for deepening their relationships with a bank.

The best part? Your digital bank can expand beyond offering just financial services and become a one-stop-shop for lifestyle products. This can cover the needs of all users now and in the future — from ordering a quick bite to saving up for a house and securing the best mortgage rate possible.

But how do banks get to this point? Below, we’ll outline some key steps you can take to develop and launch marketplace banking:

1. Define a marketplace strategy

First, it’s important to set a clear vision for your banking marketplace. You can do this by asking some important questions:

- What are your goals when developing a banking marketplace

- How will you define and measure success?

- Who is your target audience, and what are their financial needs?

- What are your direct competitors doing, and how can you offer something better?

Answering these questions will help you define your strategy, which will become the blueprint for all subsequent decisions.

2. Design from the customer, to the customer

For modern banks, UX is a key differentiator. When designing a banking marketplace, put the customer at the heart of the process. To do this:

- Use data insights — enabled by open banking or internal analytics — to understand customer pain points, preferences and behaviors

- Create a user-friendly interface that simplifies navigation across diverse offerings

- Test your prototypes with real users to ensure the experience is intuitive and solves their problems

3. Leverage open banking infrastructure

Open banking provides the technical infrastructure for marketplace banking. By tapping into open banking APIs, you can enable secure data sharing and integration with third-party providers.

Ensuring compliance with regulations such as PSD2, as well as local data privacy laws and cybersecurity best practices, will enable you to establish standardized processes that maintain trust. In addition, switching to microservices architecture will enable seamless API communication between different application layers as well as with external vendors.

4. Develop your marketplace platform and capabilities

When it comes to developing your marketplace capabilities, you have a few options. For example, you can build a platform in-house that supports a marketplace ecosystem. This could either be a standalone platform or an evolution of your current mobile banking app. You can also select from a range of pre-built, third-party solutions designed to support financial ecosystems, such as:

- White-label banking platforms

- FinTech-as-a-Service (FaaS) providers

- Enterprise marketplace solutions

- Open banking aggregators

- E-commerce platforms adapted for finance

Whatever you choose, your platform should be able to handle diverse functionalities and scale as offerings grow. Key capabilities might include AI-driven recommendations, real-time analytics for partners, and a modular architecture that allows you to plug in new services easily.

5. Build strategic partnerships

With the technical foundations in place, you can start building out your marketplace. This involves Identifying and onboarding third-party providers that complement your core offerings. For example, you can partner with:

- FinTechs lending platforms

- Insurance providers for integrated coverage

- Wealth management tools and robo-advisors

- Ecommerce and loyalty platforms

- Budgeting and personal finance tools

When building strategic partnerships, it’s important to negotiate terms that benefit all parties. Your bank gains commission or referral fees, your partners gain access to your customer base, and your users get the slick financial tools they need via one intuitive interface.

6. Pilot, test and iterate

Launch a minimum viable product (MVP) with a limited set of services to test the concept. Then, you can gather feedback from early adopters and partners, asking important questions such as:

- Did customers find the mortgage comparison tool useful?

- Was onboarding seamless for partners?

- How do UX flows compare with our competitors?

The answers to these questions will help you refine your features, fix bugs and enhance personalization before a full rollout.

7. Market the marketplace

Once you are up and running, it’s time to drum up interest. You can build awareness and trust through targeted marketing campaigns that highlight the convenience of a one-stop financial hub. The key here is to focus on real-world benefits rather than getting bogged down in technicalities. You can also leverage social media, email and in-app messaging to educate customers on how to use the platform.

8. Take action and scale

Marketplaces are dynamic by nature. With a proven model in place, you can expand your ecosystem by adding more partners and services to meet changing customer demands. As you scale, make sure you continuously monitor performance metrics such as customer adoption, partner revenue and churn rates.

Banking marketplace comparison: What digital banks are up to

The challenge for FinTech banks now is to decide which “goods” to curate in their marketplace.

Below is a comparison chart showing which services and products four of the top digital-first banks have integrated.

Financial services

|

|

Monzo |

Starling |

Revolut |

N26 |

|---|---|---|---|---|

|

P2P payments |

Instant transfers, bluetooth payments to nearby users, and bill-splitting via shared tabs. | Free bank transfers and instant Starling-to-Starling payments. Split bills and “Settle Up” feature. | Instant payments to other Revolut users, bill splitting and group expenses feature. | Free P2P payments, instant transfers to N26 users via Moneybeam, free SEPA payments. |

|

FX and foreign payments |

Free card payments abroad at the Mastercard exchange rate. Partnership with Wise enables cheap transfers to foreign bank accounts. | Free payments and cash withdrawals abroad at the Mastercard exchange rate. International bank transfers with a 0.4% fee. | Unlimited FX exchanges at the interbank rate. No-fee spending in foreign currencies. Multi-currency accounts. | Free card payments worldwide. Free ATM withdrawals abroad for certain account types. Free foreign transfers via Wise. |

|

Personal lending |

Loans of up to £25,000, overdrafts of up to £3,000. | Loans currently not available for personal account holders. Overdrafts available up to £5,000. | Personal loans up to €35,000 with flexible repayment terms. Overdrafts are currently unavailable. | Personal loans of up to €35,000 with rapid approvals. Overdrafts up to €15,000. |

|

Savings |

Instant access savings accounts with competitive interest rates, savings pots and cash ISAs. | “Spaces” savings pots, easy-access and fixed-term savings accounts, and cash ISAs. | Savings Vaults, instant-access savings accounts. | Savings accounts are available in some markets (e.g. Germany) but not others (e,g, UK). |

|

Insurance |

Home and contents insurance now available, with travel insurance also available on Max accounts. |

Mobile phone insurance, business insurance, life insurance and more via the Starling Marketplace. |

Travel, phone and event insurance via paid plans. Pay-per-day travel insurance. | Travel and electronics insurance available on premium plans, with additional coverage coming soon. |

|

Investing and trading |

Three investment funds available with different risk levels, managed by BlackRock. |

Customers can invest in investment funds, pensions and ISAs via a range of third-party providers.. |

Commission-free (within the monthly limit) trading and investing for stocks, ETFs and crypto |

Commission-free trading on stocks, ETFs and crypto, plus three actively managed funds. |

|

Finance management |

Spending analytics and trends, budgeting tools, savings pots, credit score checking. |

Spending insights, savings goals, round-ups, real-time notifications. | Budgeting tools, pockets for saving, spending analytics, round-ups, subscription tracking. | Spending categorization, statistics, savings sub-accounts (Spaces). |

Additional services

|

|

Monzo | Starling | Revolut | N26 |

|---|---|---|---|---|

|

Travel and hospitality |

Travel insurance, including luggage and lost valuables. |

Travel insurance available via third-party providers. |

Discounted or free airport lounge tickets available in-app for premium users. Pay for flights in installments. Travel, baggage and car-hire insurance also available. |

Travel, flight delay, baggage and device theft insurance. |

|

Utilities and government services |

Energy switching available. |

Energy switching available in Starling Marketplace via Bionic. |

Ultra plan comes with 3GB of global data available via an eSIM, for internet access while traveling. |

Free energy switching service available via Qwist. |

|

Lifestyle and added-value services |

Monzo Perks, cashback features and In-app charitable donations. |

Loyalty programs available via a partnership with YoYo. |

RevPoints loyalty program, regular or one-off charitable donations. |

Cashback rewards program that allows users to earn while they spend. |

The missing links in digital banking marketplaces

As the two charts above illustrate, most banks concentrate their efforts on expanding their portfolio of financial services. Some are also venturing into the utility, insurance and travel sectors. Yet, very few players are expanding beyond those areas – into the general lifestyle field.

And it’s a shame because this domain promises huge rewards. Customers can benefit from added-value services offered by their all-inclusive bank – e.g. organizing grocery delivery, securing travel insurance or signing up for a new gym in-app.

Just consider the following data:

- The global market for food delivery is worth almost $250 billion

- The global online travel market is expected to reach $838 billion by 2029

- The global wellness industry is now worth over $6 trillion

Your customers are already spending money on all those types of services. Enabling them to do so via your banking app means extra convenience for them, and an extra revenue stream for your business.

When you think of the current unicorn companies, you’ll find plenty of digital marketplaces on the list — Airbnb, Uber and Coursera to name a few. These companies did not revolutionize the industry with a brand new product per se. They capitalized on the “added value” obtained from offering a better way of connecting consumers with service providers.

As a digital bank, you can pursue a similar route — drive more value from offering your clients a better way to pick and choose the services they need.

Intellias — your partner in banking IT and technology services

Building a banking marketplace is not without its challenges. To ensure your marketplace delivers on its promise, you need to build a platform that’s robust, scalable and intuitive. Moreover, your platform must be able to integrate with open banking APIs and third-party FinTech solutions without a hitch. This is where Intellias can help.

Our expert team helps banks and financial service providers transform their IT infrastructure and deliver outstanding customer experiences. We can help you:

- Build a vibrant banking marketplace that drives growth and revenue

- Meet changing customer needs with innovative tech solutions

- Design customer-centric banking apps, tools and services

- Build a strong technical foundation for security and growth

- Boost efficiency through back-office automation

We have a proven track record of helping banks turn ideas and concepts into real-world products and services that move the needle. For example, we helped: