Customer loyalty and regulatory compliance are universal priorities for competitive businesses. Digital wallet implementation can help you meet user demand for seamless, convenient, and secure transactions. And the best part? Popular digital wallet solutions like Apple Pay and Google Pay don’t require massive investments.

However, it’s no easy task to integrate digital wallets. Companies must navigate the complex legal guidelines and technical requirements of Apple and Google. You may also need to modify your app or website to align with their UX practices.

That’s where we step in. Intellias has successfully integrated Apple Pay and Google Pay digital wallets into existing online services while ensuring strict data security and privacy regulations compliance. Alongside other projects, we helped the first all-digital German bank integrate digital wallets for contactless payments.

As you continue reading, you’ll discover more practical insights from the case studies, complete with corresponding references.

In this article, we highlight the business possibilities and best practices for integrating Apple and Google Pay into your services. But first, let’s begin with a brief industry overview.

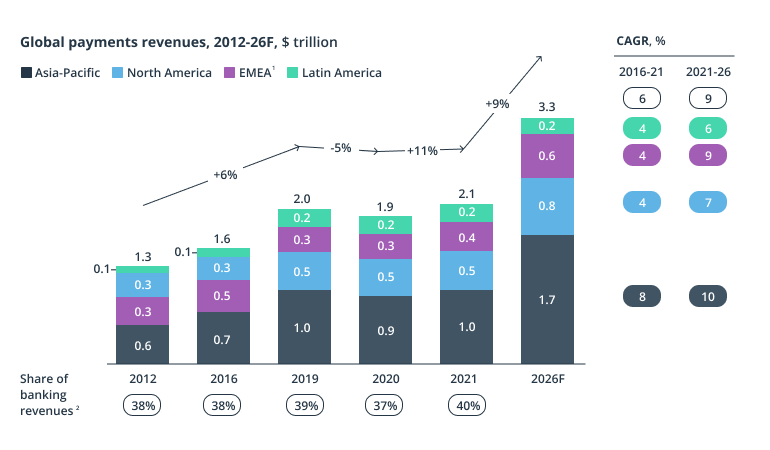

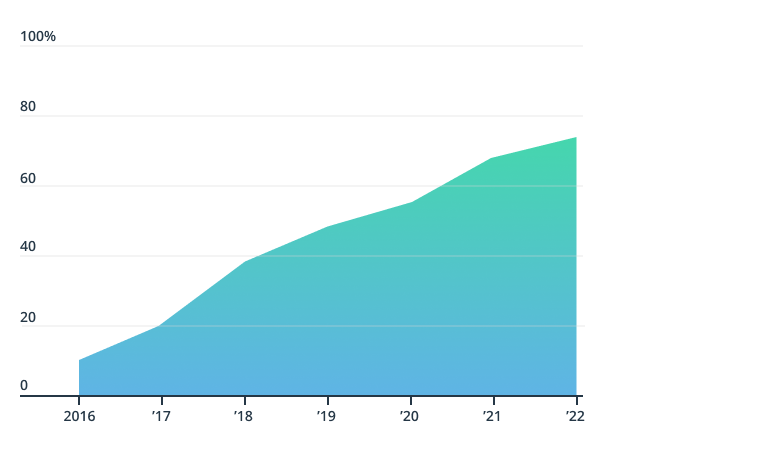

Digital wallet adoption is growing

Source: McKinsey

Digital wallet payments are skyrocketing, according to McKinsey’s 2022 Sustaining Digital Payments Growth research. The growth rate of contactless transactions was 13% per year between 2018 and 2021. In emerging markets, such as Latin America, Africa, and Asia, cashless payments have grown at a 25% annual rate.

Digitalization accelerates the transition to contactless payments. A 2022 report by Juniper Research shows there could be over 5.2 billion digital wallet users by 2026.

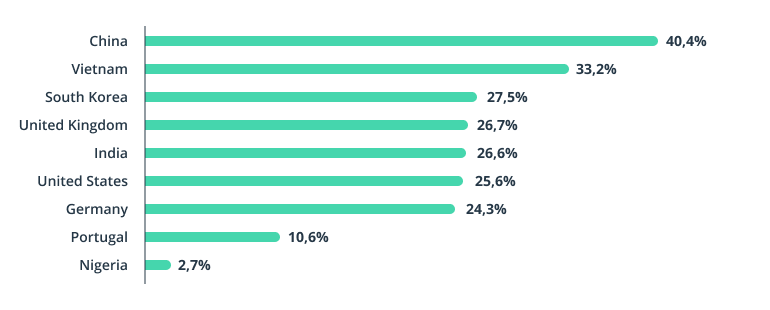

Increasing mobile wallet integration

Source: Daxue Consulting

Mobile wallets are now at the forefront of payment methods. Statista says nearly half of global e-commerce transactions were made via mobile wallets in 2022. About 2.8 billion mobile wallets are in use worldwide now.

The Asia-Pacific market accounts for over half of mobile payment wallets. A Daxue Consulting report found that around 64% of China’s population utilized mobile payments.

Globally, according to Focus on Business, up to one-third of all point-of-sale (POS) transactions will be made by mobile wallets by 2024.

The 2022 CB Insights Future of the Wallet report shows that mobile wallet usage accelerated after 2021. There are many reasons, but they primarily boil down to consumer appetites. People want to conduct transactions seamlessly and manage their finances in one place instead of on myriad banking apps.

Think about it. We carry our social lives, work, entertainment, and knowledge base in our pockets — everything’s on a smartphone now. We spend a large chunk of the day checking our mobile devices. In some countries, the number of smartphones exceeds the number of residents, which means many people own more than one device.

Mobile payment systems today simplify different forms of payments on your smartphone. The convenience and simplicity largely explain the high rates of Google Pay and Apple Pay adoption globally.

Google Pay and Apple Pay penetration rate

Apple Pay and Google Pay are the most popular digital wallet solutions. Although they are available on most iOS and Android mobile devices, many countries didn’t rush to adopt them. For example, Apple Pay and Google Pay came to Germany only around 2018.

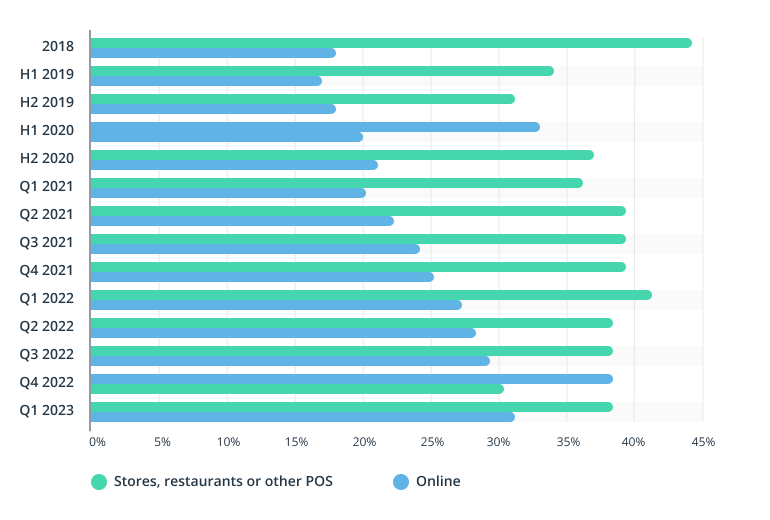

Google Pay usage for online payments and POS in the USA, 2018-2023

Source: Statista

In 2023, Google Pay works in 189 countries, with 72 directly supporting contactless payments. The number of users is hard to identify. Still, Statista shows that 80% of surveyed consumers in India used Google Pay between April 2022 and March 2023.

Source: Loup Ventures

Apple Pay mobile payments were available in over 80 countries in 2022. According to Loup Ventures, it was used by nearly three-quarters of iPhone users in the US (25% more than in 2020). Meanwhile, Apple itself says over 90% of US retailers accept their mobile wallet.

Let’s see what opportunities open up to companies that implement digital wallets. And, to dig deeper, we’ll look at why some companies haven’t rushed to adopt Apple Pay or Google Pay.

The possibilities of digital wallet integration

Incorporating digital wallets into your mobile apps and sites can redefine how you interact with customers. This comes with a wealth of business opportunities and some potential challenges.

Benefits of digital wallet implementation

Digital wallets like Apple Pay and Google Pay unlock benefits for your business and your customers. Here are some reasons you should integrate them into your services.

- More conversion opportunities. When using Apple and Google Pay, customers still get cash-back, loyalty points, and other rewards. They may also store multiple cards in a single wallet to use at different stores to maximize reward points (for example, if a specific service gives cash-back for Visa payments).

- Improved customer retention. A lack of seamless mobile payments often makes customers flip to other brands. Mobile wallet integration lets users store multiple payment methods in one app to quickly pay via sites, quick response (QR) codes, or near-field communication (NFC) terminals.

- Reduced fees and chargeback. According to McKinsey, banks partner with Apple Pay and Google Pay to avoid processing the delivery of funds, ultimately reducing their operating costs. According to Google, digital wallet transactions have much lower chargeback rates than traditional card transactions.

- Expanded customer insight opportunities. Digital wallet implementation doesn’t cut you off from customer data. You can segment your user base and target them with personalized strategies based on their purchasing behavior and preferences.

- Secure infrastructure for payments. Apple and Google provide a more secure infrastructure than traditional transactions. They tokenize every transaction, replacing it with a unique anonymized code so users don’t display their credit card or personal information.

- Lower risk of fraud. The payments are also protected with biometrics: their passcode, touch verification, or facial recognition. If a customer loses their smartphone, there is less chance of criminals conducting transactions.

Challenges of implementing digital wallets

The implementation is not without its complexities. There are still things you ought to consider despite Google and Apple Pay’s popularity.

- Lower consumer uptake in some regions. Mobile wallet payments aren’t popular in emerging countries and rural areas. Based on McKinsey’s data, cash remains the top POS method in Africa (95% of transactions in 2021), Thailand (63%) and Indonesia (51%).

- Requirements from Apple and Google. Apple and Google require your sites and apps to follow strict technical specifications and UI/UX requirements. They also prohibit using their wallet integration services for certain types of products or currency transfers (unless they are specifically approved by Apple or Google).

- Rising privacy concerns. Digital wallet solutions can store multiple payment types, which increases the risk of malware attacks and data leakage. Companies need their apps to comply with Customer Due Diligence (CDD), Strong Customer Authentication (SCA), Payment Services Directive 2 (PSD2), and other security regulations.

- Complexity of integration. Your team must integrate various technologies (like NFC and biometrics), ensure interoperability with POS terminals and networks, and maintain high system reliability. Even with APIs and SDK kits, the process may lead to issues that can disrupt the existing interface or app functionality.

Now, let’s consider how digital wallets work and what is required for their implementation.

Google Pay vs. Apple Pay: How they work

Apple Pay and Google Pay have minor differences in their processes and feedback mechanisms. Here’s how they work for users.

- Adding a payment method. Apple and Google Pay support credit cards, debit cards, PayPal accounts, and other payment systems. After verification by the payment system, the payment method is added to the digital wallet.

- Initializing the transaction. Customers can pay by tapping their mobile devices or wearables on POS terminals, scanning QR codes, or online shopping. The wallet tokenizes the transaction and generates a temporary security code.

- Request processing. The security token and unique code are sent to your payment system (like your bank), which forwards it to the payment network (like Visa or Mastercard).

- Payment confirmation. The transaction is approved without the merchant reading the customer’s payment information.

To implement Apple’s or Google’s contactless digital wallet, merchants only need an NFC-based POS terminal or a printed QR code. How hard can it be to integrate these into your business?

Both Google Pay and Apple Pay have a set of requirements for financial institutions to follow if they wish to support these payment services. This way, Google and Apple ensure their services work consistently on every website, app, and device.

Google Pay implementation

Here are the essential steps of Google Pay digital wallet implementation:

- Get a Merchant ID. Sign up with the Business Console to generate a unique identifier for your business.

- Apply for production access. You need to make sure you have a compliant gateway, server environment that meets the PCI DSS standards, and domains qualified to call Google Pay API.

- Implement the APIs. At this step, you should declare the version of the Google API, load the libraries, and integrate the Google Pay button into the UI (according to Google’s requirements).

- Approval and launch. You should submit the integration via the Business Console and wait for Google’s team to approve it.

For more information about the requirements, read the Google Pay guidelines.

Apple Pay implementation

The Apple wallet implementation process isn’t that much different.

- Get a Merchant ID via the Apple platform. This will act as your unique signature for Apple Pay transactions.

- Create a payment processing certificate. The certificate is a public key designed to encrypt payment details transmitted to Apple’s servers.

- Activate Apple Pay in Xcode. You must add your Merchant ID and Apple Pay entitlement to your app’s capabilities in Apple’s integrated development environment.

- Optimize for the web app. To authenticate Apple Pay for your website, you should create a Transport Layer Security (TLS) certificate associated with your Merchant ID.

You can access the Apple Pay setup documentation for more information.

How we provide wallet integration services

Intellias provides software engineering, consulting, and modernization services to financial companies across Europe. Here are a few examples of how we have helped integrate digital wallet solutions and create mobile finance apps from scratch.

Google Pay and Apple Pay implementation for contactless payment

A German-based bank wanted to incorporate Apple Pay and Google Pay into their platform. This was when Apple Pay was just entering the German market. We had to follow the strict implementation standards alongside intricate regulations.

- Intellias engineered a cohesive solution integrating both Apple Pay and Google Pay wallet into the client’s app.

- To ensure the robust protection of cardholder data, we maintained compliance with the PCI DSS.

- Our team initiated a tokenization mechanism to transmute sensitive cardholder data into anonymized codes.

- The banking apps were to align impeccably with Apple’s and Google’s stringent UX criteria.

- We fine-tuned Google Pay for one-tap and two-tap payment scenarios.

Implementing Apple Pay and Google Pay helped the client expand the client’s payment options while keeping the platforms secure against potential data breaches.

Digital wallet for QR payments

Our client wanted to merge their QR payment expertise with Alipay to pioneer a robust contactless payment landscape in Europe. We had to research the backend of the Alipay platform and adapt the system to their requirements to start the integration.

- Our team built a QR code-centric payment system compatible with European banks, e-wallets, payment platforms, and retailers.

- The system required users to link their bank accounts only once.

- We prioritized user security and privacy, ensuring that personal data and banking specifics remained anonymous during transactions.

In the end, we created a transformative mobile QR platform that integrated digital wallets in Europe with Alipay. Additionally, the app reduced the client’s costs for POS equipment.

A custom mobile banking system

Germany’s first digital-only bank wanted to offer a mobile-only banking system for local telecommunication providers. We were to reinforce the client’s internal team to implement client-centric mobile app features for secure payments and money transfers.

- Our team leveraged a Banking as a Service (BaaS) model, and the entire system was built using Ruby on Rails architecture to accelerate the development.

- We helped develop an app that lets customers set accounts using Mastercard and Visa cards via smartphones.

- With our help, the client’s team implemented a groundbreaking 60-second P2P Instant Transfer feature that enables swift money transfers through phone, social platforms, and email.

- We built a personal finance management tool with real-time analytics and an intuitive visualization of customer expenses.

This mobile banking solution now serves a vast clientele with myriad financial services — from cash transfers to emergency loans. It also automates expense categorizations, identifies spending patterns, and offers saving opportunities. As an added perk, users get 1MB of mobile data for every Eurocard transaction.

An all-in-one personal finance app

Swiss residents have many accounts, including credit, loans, insurance, and other services. A pioneering fintech company wanted a cutting-edge app to help their clients manage their personal finances.

- We upgraded the client’s platform into robust personal finance software with an intuitive mobile app.

- The app collected and classified expenses from third-party financial institutions, so the customers didn’t have to waste their time sorting through data.

- Our team integrated a convenient AI budgeting tool that forecasts the customer’s expenses for the upcoming month.

- To enhance security, we adopted a two-factor authentication system that aligns with PSD2 regulations.

Our app for iOS and Android has captured a large share of personal finance users in Switzerland. We also added an extra layer of engagement with gamification elements that give users points for in-app activities.

The future of digital wallet solutions

Digital wallets are poised for further advances in reach and functionality due to evolving consumer preferences and innovative technologies.

- Mobile wallets are expanding their features to seek more revenue streams. For example, China’s Alipay and WeChat wallets have expanded into hotel booking, gaming, and delivery services. Similarly, PayPal launched a US app in 2021 that allows managing personal finance and banking (in addition to mobile wallet functionality).

- Rise of larger digital wallet ecosystems. Digital wallets may transition into digital banks or build fintech super-apps to compete with Apple Pay and Google Pay digital wallets. These ecosystems will leverage their expansive user networks to offer a broader range of financial services.

- Companies will offer personalized advisors. These AI-powered financial assistants will help customers manage budgets, save costs, and reach other financial goals. Pioneers in this realm include Betterment, SigFig, and Empower (formerly Personal Capital).

- Blockchain integration will become more common. As pointed out by McKinsey, companies can integrate blockchain — a decentralized ledger for crypto-based transactions — to reduce transaction fees by eliminating the need for third-party intermediaries.

- Mobile wallets as digital signatures. With the potential to store everything from state IDs to medical records, digital wallets might double up as tools for both public and private service authentication. For example, the digital IDs for Apple Wallet.

- QR codes will become more popular. Mobile payments using QR codes are widespread in China (as shown in the Daxue Consulting report). Unlike NFC terminals, you only need a piece of paper or an image to initiate a payment. The unparalleled convenience means QR codes are likely to expand to other regions.

- Digital wallets integrated with IoT. CB Insights forecasts that the global wearable payments market will reach $1.3 trillion by 2028 (up from $285 billion in 2019). Apple, Google, and Samsung already pair their wallets with smartwatches for seamless payments.

Embracing these trends will be critical for your business and your customers. It’s often worth finding a trusted partner to help you stay ahead of the curve.

Integrate Google Pay and Apple Pay for seamless payments

As popular as mobile wallets are, they’re about to get even more popular. They will include more integrations and functionality, evolving from contactless payment mechanisms to something more akin to a fintech super-app.

Apple Pay and Google Pay mobile payment platforms are the frontrunners due to their reliability. Integrating them into your platform can be complex, as you need to meet stringent technical, UX, and security standards. Collaborating with experienced partners is often the best way to successfully implement digital wallet services.

Intellias has years of experience elevating our client’s platforms and creating custom digital wallet projects. Contact us to see how we can bring Apple Pay and Google Pay functionality to your app or website.