The banking sector has a lot of external stressors: regulatory pressure, TechFin and FinTech competition, and rising customer demand for faster/better/cheaper services. To put out all those fires, banks often resort to patches. But a quick interface fix here and an app improvement there won’t change your odds of success in the long run. To stay profitable in the 2020s, banks need to look straight into their core systems.

46% of bankers see these legacy systems as the biggest barriers to the growth of commercial banks.

The case for modernizing financial legacy software systems

As we mentioned in our first post about digital innovations in banking, pioneering new customer-facing solutions is just one piece of the puzzle. To support those new solutions, you’ll also need to modernize your legacy systems.

Legacy banking software, lovingly dubbed “the next financial crisis” by some industry analysts, is a major constraint, preventing traditional banks from attaining the same rapid product scaling capabilities as more nimble digital banks have.

The word crisis may sound strong. But when you look at the data, crisis may be an understatement:

IBM released its flagship System/360 back in 1964. Today, 92 of the world’s top 100 banks still rely on these 50-year-old IBM mainframes.

On average, larger incumbent banks can now have 20+ different core legacy banking systems at their disposal. Unraveling these setups becomes more challenging over time, as most were written in COBOL — a trendy programming language in the 60s and 70s. As you might guess, finding a COBOL programmer these days isn’t easy, since most are enjoying a happy retirement.

What’s even more aggravating is that it’s hard to identify how new code (e.g. Java) or new tech (e.g. cloud technology) will interact with older COBOL systems. These factors make it hard to gauge where an integration issue may arise.

As a result, some banks end up being powered by so-called spaghetti connections — a setup where every system element is connected to everything else, and pulling one string can create a crippling operational knot.

But despite being one very expensive plate of spaghetti — legacy financial systems eat up 60% to 80% of banks’ total IT budgets — few banks are rushing to modernize their systems.

But here’s the deal:

With every new feature that you are adding to the existing system, you are making migrating off that system harder.

So how can you muster the strength (and gain buy-in) for a legacy systems modernization project?

Start by building a strong roadmap, clearly showing which financial systems should be unbundled first and demonstrating the risks and potential gains.

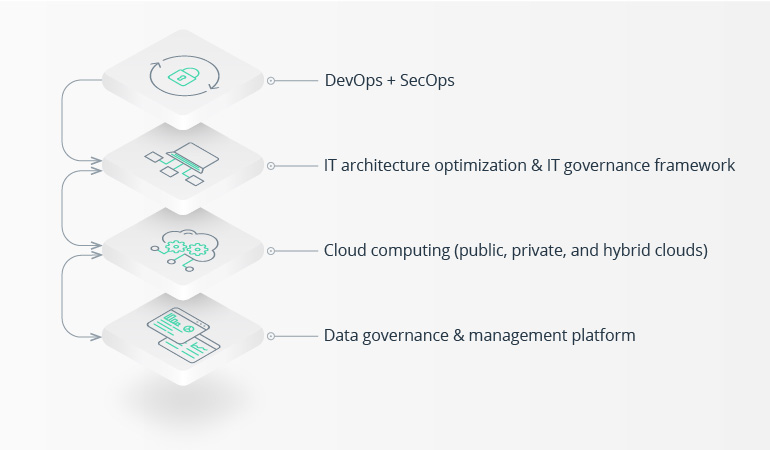

4 priority areas for backend banking transformations

1. Data governance & management platform

In 2020, financial data can reside anywhere thanks to cloud technologies. Yet it remains stranded in legacy systems. Or uncollected for the lack of ability to do so in real time.

As a result, incumbent banks cannot compete with digital players in terms of personalized up-sells/cross-sells/advertising, cannot deploy innovative analytics-driven solutions such as personal finance management or coaching apps, and cannot experiment with predictive analytics, artificial intelligence (AI), and machine learning.

As Luis Moreira-Matias, the Head of Data Science at Kreditech, said in :

Personalization or the ability to make the right offer at the right time — either to grab a customer or to make a profit out of them — is a key factor for banks to increase customer lifetime value. Such personalization is impossible without big data analytics and data science.

Neither can incumbent banks embrace real-time business intelligence and move towards advanced big data analytics without having a strong data management platform.

Moreover, shifting to a unified data platform can majorly improve data traceability, accountability, and, subsequently, reporting capabilities to help banks stay compliant with the latest industry regulations. It also can make payment system architecture more resilient to security vulnerabilities.

To capture this host of benefits, your data governance framework should strongly align with a wider IT governance framework (discussed in the next section).

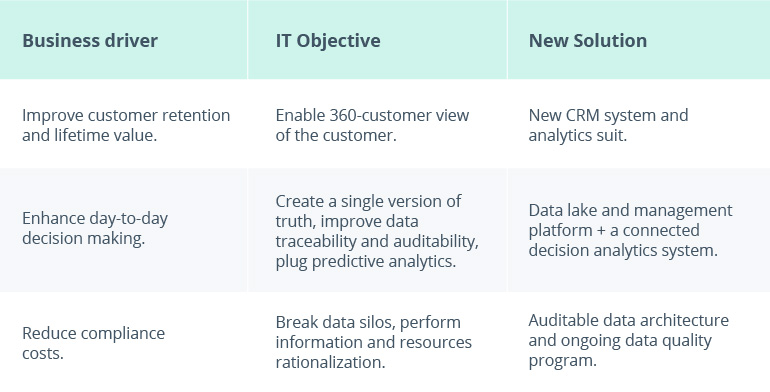

One way to do this is to map each business driver to a respective IT objective and then to a technical solution. For example:

2. Cloud migration and transformations

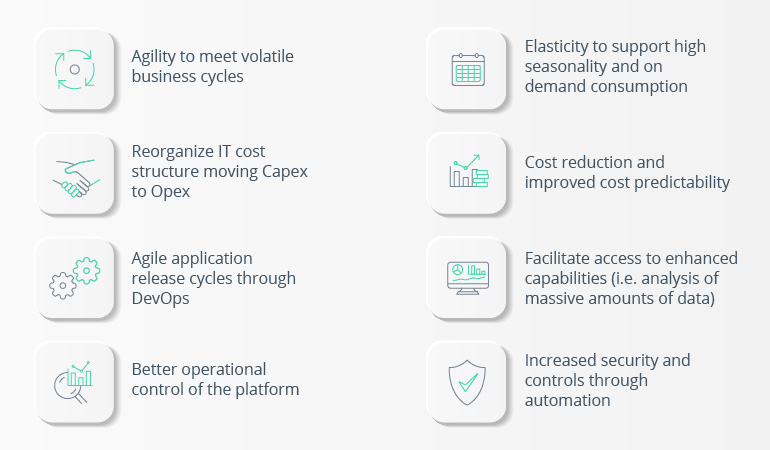

Cloud computing has made significant leaps in terms of efficiency, affordability, and security, resulting in a host of new opportunities for banks:

Source: Accenture — Moving to the Cloud: A strategy for banks in North America

Replacing struggling on-premises legacy systems and breaking away from the costly equipment replacement/upgrade cycle is one obvious reason for migrating to the cloud. Indeed, the total cost of ownership ends up being attractive for most financial institutions.

Apart from causing this major shift in IT spending, the cloud empowers banks to grow and scale through the consumption of external services connected via APIs.

Rather than building a new product from scratch, you can seamlessly integrate existing solutions from vendors and other FinTechs. Or you can go a step further and start assembling an ecosystem of financial and non-financial products available to your customers via a single interface to embrace the marketplace banking model.

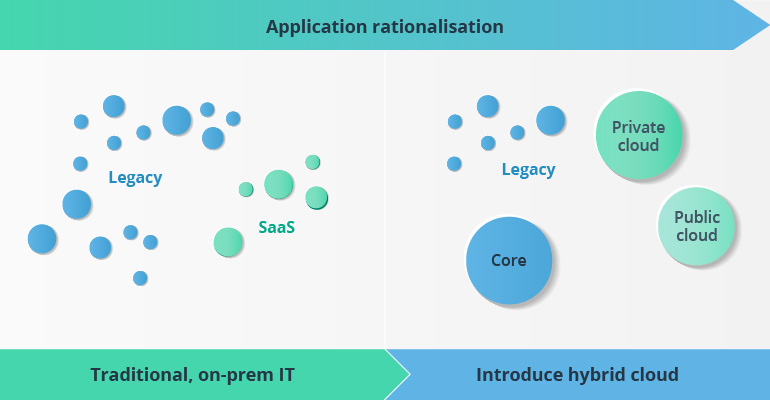

The best part? You can attempt gradual IT modernization, bringing one element of your legacy systems to the cloud at a time, as Deloitte suggests.

Source: Deloitte — Getting cloud right: How can banks stay ahead of the curve?

Shifting towards a portfolio of cloud services and delivery models (SaaS, IaaS, and PaaS) can help you gradually unbundle your legacy software without causing major operational disruptions.

Depending on your business priorities, you can pick and choose your cloud battles. For instance, Credit Suisse partnered with Cloudera to launch an enterprise-wide big data analytics platform rather than building all the infrastructure from scratch, achieving a 38% reduction in total cost of ownership and faster access to cutting-edge analytics capabilities.

Ultimately, the key to reaching the cloud is having a clear roadmap that includes the following steps:

- Laying a cloud foundation. This is your launching pad for new solutions. Specifically, you’ll need to conduct a preliminary assessment of your infrastructure needs as well as your security, legal, and compliance requirements.

- Assessing your app portfolio.Next, you’ll have to determine and line up the best candidates for migration. To do that, you’ll need to conduct several application discovery and dependency mapping sessions, perform an application migration path analysis, and build up business cases for shortlisted candidates for migration.

- Planning your migration. Once you have a prioritized list of candidates, you should finalize the target application architecture layout, create a detailed migration plan, and run a small-scale pilot.

- Executing the migration.This involves the migration itself, plus all the subsequent integrations.

- Conducting testing and acceptance. Test and validate all the migrated workflows and conduct comprehensive quality assurance checks to ensure proper performance.

Clearly, the actual process of cloud migration will be more complicated, as some legacy apps will need to be refactored or re-engineered from scratch.

No two cloud journeys are the same, so it’s best to have a team of cloud consultants on your side advising you on the optimal migration candidates.

3. IT architecture optimization and improved IT governance

Fully stepping away from the legacy core isn’t feasible for most banks, as the risks are too high. What are the alternatives?

Introducing gradual decoupling and adding modularity in your IT architecture. Going back to the spaghetti analogy, you have to start pulling out those noodles and reorganizing them on your plate!

Granted, banks today have the technological opportunity to carry out IT modernizations without causing major operational disruptions by choosing to decouple and modernize certain elements of their systems rather than replace them in one fell swoop.

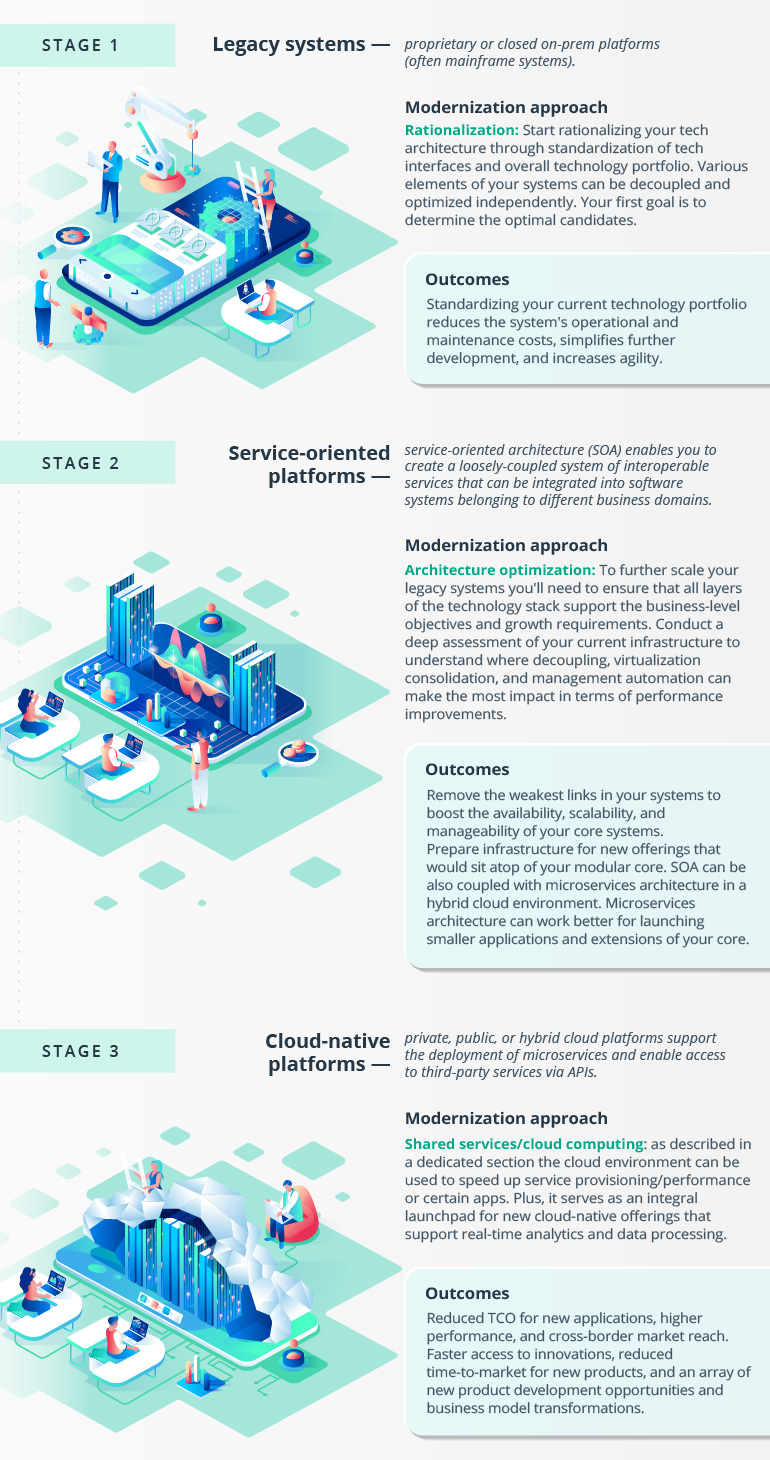

Broadly speaking, core banking platforms fall into three evolutionary stages. You can choose to either perform modernization at the system level or attempt to evolve from one stage to another.

Having a strong IT governance process is the key to making this evolution happen. In particular, you should focus on:

- creating strong alignment between your business objectives and technical capabilities for supporting them

- eliminating redundant and overlapping systems (supported by legacy infrastructure and technology) and replacing them with new tech

- developing a standardized technology portfolio that’s easier and cheaper to maintain in the long run

- implementing a unified approach to risk, compliance, and security management.

4. DevOps and SecOps

While legacy systems need to be decoupled, the software development process, on the contrary, needs to be unified for greater performance gains.

Bridging your development, operations, and quality assurance is what DevOps is all about. DevOps practices can help you shorten the time to market for new products without compromising their quality.

Key principles of DevOps:

- Shift left — Introduce more OPs and quality assurance during the early stages of the software development lifecycle to minimize the risks of costly rework later on.

- Automate — Systematically automate the development and delivery pipelines to minimize bottlenecks and increase the workflow speed. Target repeatable and reliable processes first.

- Measure and monitor — Keep a close eye on core software metrics that act as proxies for process and product quality: delivery lead time (proxy for speed), deploy frequency (proxy for batch size), mean time to recover (proxy for adaptability), change failure rate (proxy for quality).

- Assure continuity — Strive for continuity in both delivery and learning. Collect feedback, review metrics, and continuously invest in additional process improvements.

Just what type of improvements can banks gain from DevOps? Tata reports that one global bank managed to cut their SDLC time by 47% and reduce the time to market to 6 months (from 12 to 15) for one new credit card product after implementing an API strategy built with DevOps practices.

SecOps is the next step for banks who aim to meet the security by design compliance requirement. By adding security testing early in the application development lifecycle, you can majorly minimize the risks of security incidents within deployed products (and subsequent costly penalties!).

Beyond backend transformations: Adding new tech blocks to your bank

Transforming your backend operations and modernizing core legacy technologies is no easy task. But it’s an integral step in your journey of transformation.

Without a better core, you won’t be able to bank on bigger innovations such as:

- AI/ML-powered decision analytics engines for banking personnel

- Innovative credit card scoring models powered by big data analytics

- Improved fraud detection with predictive analytics and ML

- A happy combo of AI and blockchain pilots

After all, going after other innovations in the financial space that are essential to staying competitive and profitable in this decade.

When you factor in all the performance, operational, and ultimately revenue gains, it becomes clear that modernizing legacy systems isn’t too costly. Rather, it’s too expensive to postpone it any further!

Let’s unravel your spaghetti systems together! The Intellias team can help you determine the best candidates for modernization and develop an initial modernization roadmap. Contact us to get started!